An indemnity clause is a provision in a contract where one party (the indemnifying party) agrees to compensate the other party (the indemnified party) for certain losses, damages or liabilities that may arise during the course of the agreement.

It is effectively a legal promise to protect.

The indemnifying party is basically saying to the indemnified party that “If something goes wrong and you suffer a loss because of it, I’ll cover those costs”.

Indemnity clauses are used to:

A broad indemnity clause like the above can pose serious risks to the Consultant, both legally and financially.

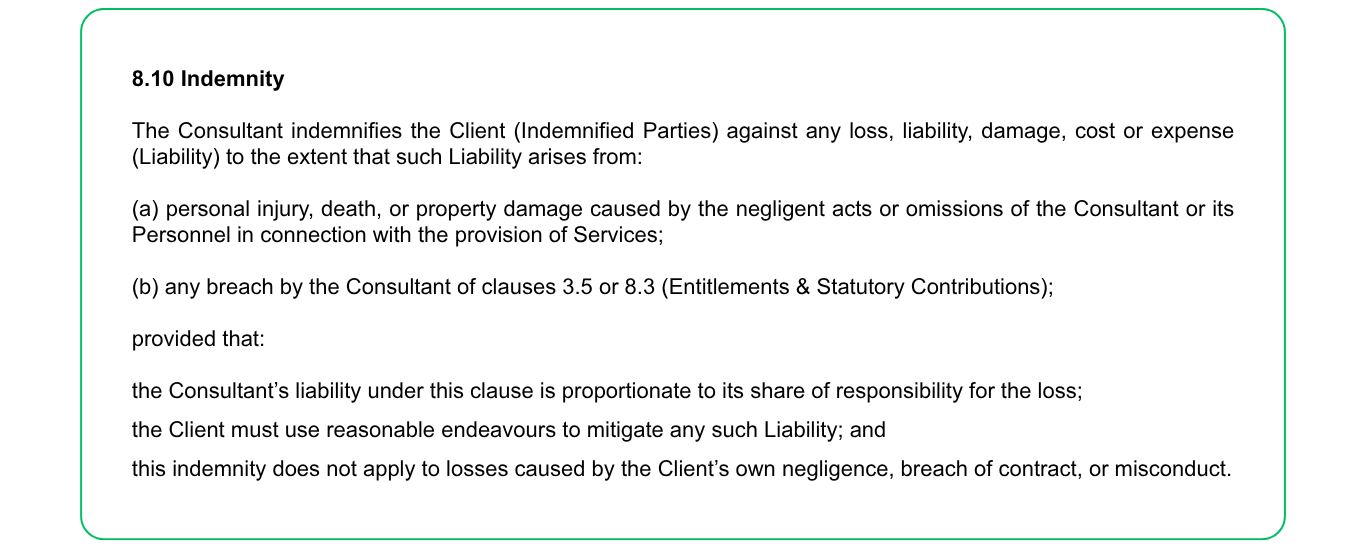

This clause covers all claims for personal injury, death, and property damage, including those made by third parties like workers compensation insurers. This means the Consultant could be liable for events beyond their control, even if they were not directly at fault.

The clause renders the Consultant responsible for the actions of their employees or subcontractors, even if those individuals act negligently or in breach of the contract.

Most professional indemnity and public liability policies exclude cover for contractual indemnities. If the clause extends liability beyond what the Consultant would normally face under common law (e.g. negligence), the insurer is entitled to decline cover.

While the clause includes a carve-out for proportionate liability, it is qualified and might not fully protect the Consultant. Courts may interpret this narrowly, especially if the indemnity overrides proportionate liability legislation (which can happen in NSW under the Civil Liability Act).

The phrases “associated with” or “in connection with” are broad and vague. This can lead to disputes over what types of claims are covered. Such disputes can potentially become costly litigated proceedings.

The Indemnity clause requires the Client to use “reasonable endeavours” to mitigate liability, but what “reasonable endeavours” are is open to interpretation; it is subjective and difficult to enforce. If the Client fails to mitigate, the Consultant may still be held liable unless they can prove that the Client was negligent in its failure to mitigate.

At first glance, a broad Indemnity clause in your favour might sound fantastic.

However, a broad indemnity clause has the potential to be unfair. In ACCC v JJ Richards & Sons Pty Ltd [2017] FCA 1224, the ACCC found that a broad one-way indemnity was unfair because it did not require fault on the part of the indemnifying party and it covered losses that could have been avoided or mitigated by the indemnified party.

Australia’s Unfair Contract Terms (UCT) regime, under the Australian Consumer Law (ACL) took effect from 10 November 2023, making it illegal to include, propose or rely on unfair terms in standard form contracts with consumers and small businesses. The reforms impose hefty penalties for non-compliance, which were not previously in place. The regime presently applies to standard form contracts for small businesses with fewer than 100 employees or an annual turnover of less than $10 million. A court can declare an unfair term void and impose penalties such as financial penalties, injunctions, or orders to compensate affected parties.

In a recent claim, the Policyholder had a contract in place with the Principal Contractor (a property manager) to perform services as required in accordance with the Principal Contract.

On this occasion, the Policyholder had subcontracted on an informal basis with a Technician to perform works on the Policyholder’s behalf under the Principal Contract. Unfortunately, the Technician made an error during the works which caused damage to the property managed by the Principal Contractor.

The Principal Contractor pursued the Policyholder for damages pursuant to the contract.

The Policyholder submitted the claim to its Liability Insurer. For relationship reasons, the Policyholder did not pursue the Technician for the damage.

The Insurer, having reviewed the claim, deemed the Technician to be 30% liable and the Policyholder 70% liable for the damage.

However, based on a broad indemnity clause written into the contract in favour of the Principal, the Insurer applied the Contractual Liability exclusion against the Policyholder which had the effect of the Policyholder having to bear 30% of the claim. That 30% was deemed to be the Technician’s liability. The Insurer paid 70% of the quantum of the claim, which represented the Policyholder’s negligence, leaving the Policyholder 30% out-of-pocket due to the Contractual Liability exclusion. This is an example of how an indemnity clause that is incompatible with the insurance policy can leave a policyholder exposed to an uninsured loss.

If you have any concerns with your contracts, we recommend consulting your legal adviser to tailor them to your needs.

.png)